Bond Market Wary of Fiscal Credibility

The US bond market is moving closer to a reckoning over President Donald Trump’s economic damage, with Treasury yields still elevated, the curve steepening modestly and credit spreads offering only limited protection if fiscal and policy credibility keeps eroding.

That matters because the bond market is usually the first place investors price whether a government can keep borrowing costs contained. The 10-year Treasury yield, at 4.57% on the latest reading and forecast at 4.561%, remains far above the levels that prevailed when the Fed pinned rates near zero, while the 2s/10s spread has narrowed to 0.37 percentage point. In other words, investors are demanding a meaningful term premium even as recession signals remain mixed, suggesting the market is not yet in panic but is no longer offering Washington the benefit of the doubt.

The most important implication is fiscal. Higher long-end yields raise the government’s refinancing bill, tighten financial conditions and eventually feed through to mortgages, corporate borrowing and equity valuations. If tariffs, policy uncertainty and political pressure undermine growth without restoring fiscal discipline, the bond market’s patience could wear thin quickly. That would force a choice between easier monetary policy and a credibility-preserving rise in real yields, a trade-off that has historically hurt risk assets.

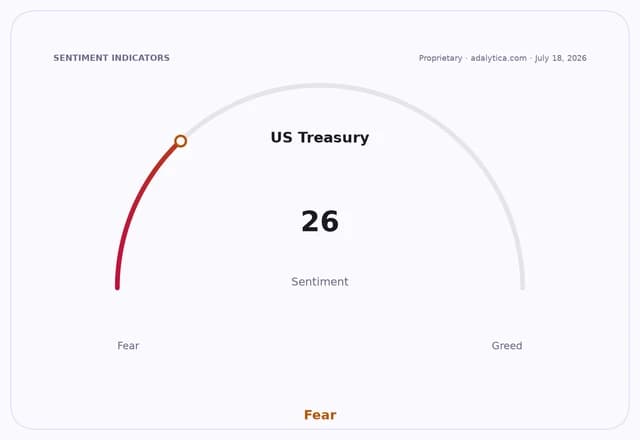

The latest market action shows how delicate the balance is. TLT, the long-duration Treasury ETF, closed at 84.52, below its 200-day moving average of 86.03, while its RSI was 19.4, a conventional technical indicator that points to an oversold market. Adalytica’s US Treasury Bonds Trade Signals also show sentiment at 26, labelled Fear, even though awareness is only Neutral. That combination suggests investors are uneasy about duration but have not yet stampeded out of the market.

Equities are still holding up, but not comfortably. SPY closed at 743.29, just above its 50-day moving average of 743.23 and well above its 200-day average, indicating the broader stock market remains in an uptrend. Yet the latest Adalytica reading on the S&P 500 has sentiment at 51, Neutral, down 18 points on the day and 49 points over 30 days, a sign that confidence is softening even as prices have not broken decisively. That leaves room for a sharper repricing if bond yields climb further or if long-duration assets start to discount slower growth and higher discount rates at the same time.

The dollar picture is less straightforward. The USD ETF dropped to 82.26, far below its 50-day moving average of 96.61 and with RSI at 43, reflecting a weaker greenback despite Treasury yields staying relatively high. Adalytica’s dollar sentiment is Neutral at 44 and has fallen 56 points over 30 days. A weaker dollar can cushion some of the inflationary effect of tariffs, but it also hints that investors are questioning US policy premium rather than rewarding it.

The bear case for the bond market is that tariff-driven inflation, larger deficits and policy unpredictability eventually push yields higher regardless of growth concerns. The bull case is that slower activity and weaker confidence force a flight back into Treasuries, lowering yields before financial stress spreads. For now, the market is sitting between those outcomes: not in outright revolt, but no longer comfortably financing Washington at cheap rates.

For investors, the key watchpoint is whether the 10-year yield can stay anchored near the mid-4% range while equities hold near record territory. If it cannot, the first casualties will be duration assets, richly valued equities and any borrower relying on stable long rates. If it can, Trump’s economic damage may remain a political problem rather than a market one. The risk is that bond investors decide they have waited long enough.

| Entity | Gains | Losses |

|---|---|---|

| Treasury buyers | ▲Higher yields | ▼Price losses on long duration |

| Treasury borrowers | ▲Cheap financing if yields fall | ▼Rising debt-service costs |

| Equities | ▲Easier if yields stabilize | ▼Valuation pressure if yields rise |

| Dollar bears | ▲Weaker USD trend | ▼Stronger dollar if risk aversion spikes |