China Airpower Boost Supports Defense Stocks

China’s increasingly advanced J-16 fighter production is another reminder that Beijing is not just expanding its air force — it is sharpening a long-range deterrence toolkit that raises the stakes across the Western Pacific.

That matters because the J-16 is not a symbolic showpiece. It is a heavy, multi-role combat aircraft built for patrols, strike missions and air superiority, the kind of platform that helps China sustain pressure around disputed waters and probe rival defenses at scale. When paired with China’s wider push into satellite-jamming and anti-space warfare, the message is clear: Beijing is investing in layered capability, not isolated headline weapons.

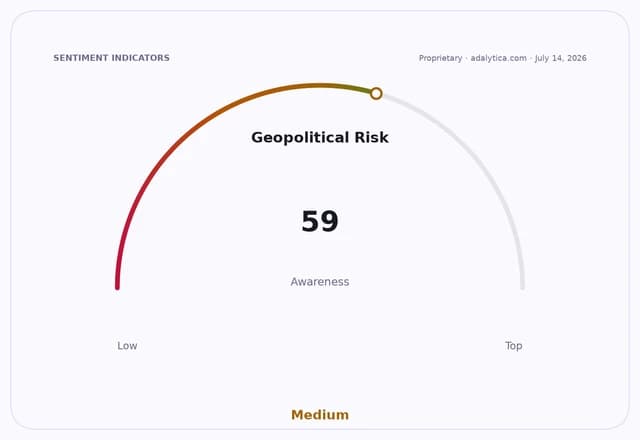

For investors, the market still underestimates how persistent this military modernization cycle is likely to be. Geopolitical tension is no longer a temporary tailwind for defense spending; it is becoming a structural budget driver. The Adalytica U.S.-China Relations gauge shows extreme fear even as awareness remains elevated, while the Global Stability indicator is also flashing extreme fear. That is the kind of backdrop that keeps procurement pipelines open, accelerates modernization, and supports a longer runway for defense contractors with exposure to aircraft, sensors, missiles, command systems and space resilience.

The strongest public-market beneficiaries remain the obvious toll roads of rearmament: Lockheed Martin, Northrop Grumman and RTX. Their shares have held up despite volatility, and the recent technical setup suggests investors are still willing to pay for hard-defense exposure. Lockheed sits near its 50-day moving average after recovering from a sharp spring drawdown, while RTX has regained momentum and is trading above both its 50-day and 200-day averages. Northrop has also stabilized from a steep selloff, a sign that the market is beginning to price in a more durable demand cycle rather than a one-off geopolitical spike.

The more important point is that China’s air and space modernization is not occurring in a vacuum. The Pentagon, allied air forces and Asian partners are being pushed toward faster spending on fighters, air defenses, electronic warfare, satellites and missile-warning systems. Every time Beijing demonstrates greater reach, the West responds with more capex. That creates a multi-year earnings opportunity for companies that sell the infrastructure of deterrence, not just the hardware.

I believe the market is still too focused on near-term budget headlines and not focused enough on the compounding effect of regional arms competition. If China keeps advancing its patrol aircraft, anti-satellite tools and integrated airpower doctrine, the beneficiaries are not just fighter-jet primes but the broader defense ecosystem: missile defense, aerospace electronics, secure communications and space-related contractors. The better trade is to own the picks-and-shovels of strategic rivalry before the next budget cycle catches up.

For investors, that means staying overweight quality defense names and treating pullbacks as accumulation opportunities. The J-16 story is not about a single jet; it is about the next phase of a global militarization cycle that can keep defense demand elevated for years.

| Entity | Gains | Losses |

|---|---|---|

| Lockheed Martin, Northrop Grumman, RTX | ▲Higher modernization demand | ▼None near term |

| U.S. and allied defense budgets | ▲Faster procurement urgency | ▼Fiscal flexibility |

| China’s PLA Air Force | ▲Expanded patrol reach | ▼Higher regional pushback |

| Geopolitical stability | ▲None | ▼Further deterioration |