China-Russia Patrol Boosts Geopolitical Risk Premium

China and Russia have wrapped up naval maneuvers and moved into a joint patrol in the Pacific, a reminder that the world’s two biggest revisionist powers are willing to turn military coordination into a more routine feature of the security landscape. For investors, the significance is not the patrol itself so much as what it signals: a deeper strategic alignment that can keep geopolitical risk elevated, complicate trade routes, and add another layer of uncertainty for global markets.

That matters economically because prolonged military cooperation between Beijing and Moscow reinforces the kind of bloc politics that can fray supply chains, harden sanctions regimes and keep defense spending rising. The Pacific is not just a map feature; it is a corridor for energy flows, manufactured goods and semiconductors, and any show of force there raises the odds of friction around shipping lanes, alliance commitments and regional defense postures. In a world already shaped by tariff threats and weaker trust between major powers, this kind of coordination increases the premium investors should assign to stability.

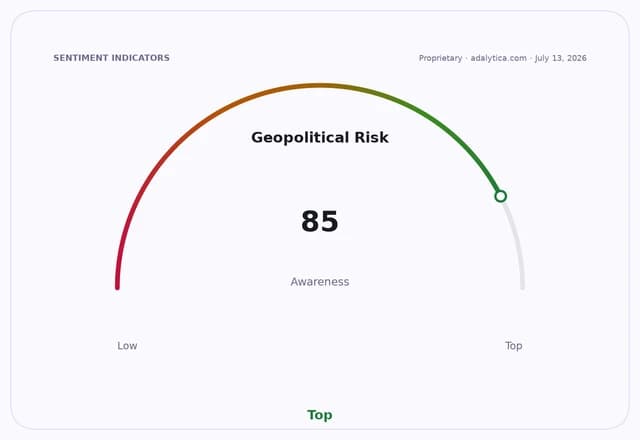

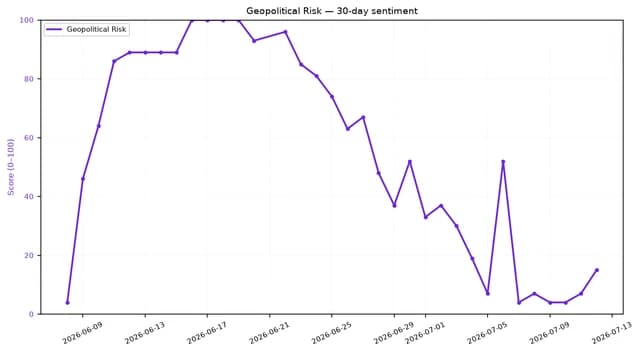

The market backdrop shows how sensitive investors are becoming to that premium. Adalytica’s Global Stability Sentiment gauge has slid into “Extreme Fear,” while its US-China Relations Sentiment has also sunk to “Extreme Fear,” with awareness still high. That combination says investors are paying close attention even as confidence deteriorates. In practical terms, that tends to support assets tied to defense, energy security and supply-chain resilience, while keeping pressure on businesses exposed to Asia-Pacific trade disruption, cross-border manufacturing and shipping costs.

The message is especially relevant for long-term investors who think in years, not days. China and Russia are not likely to unwind their strategic partnership anytime soon, and joint patrols suggest the relationship is moving beyond symbolism into repeated operational cooperation. That does not automatically mean immediate market damage, but it does mean geopolitical risk is becoming more structural than episodic. Investors should expect more headlines that can jolt sentiment, particularly in sectors with direct exposure to the Pacific and to U.S.-China relations.

Exchange-traded funds tied to emerging markets also reflect that caution. The iShares MSCI Emerging Markets ETF has softened recently, while the iShares MSCI United Kingdom ETF has held firmer, underscoring how capital can rotate toward perceived safety when global tensions rise. For diversified portfolios, the lesson is not to try to trade every geopolitical headline, but to stay broadly balanced, own durable businesses with pricing power, and be selective about regions and industries that depend on an easy global trading environment.

For investors, the patrol is worth watching because it is part of a larger pattern: the world is getting more fragmented, not less. That tends to favor companies and sectors with strong moats, reliable cash flow and less dependence on a perfectly calm geopolitical backdrop. If you are building wealth over the next 3 to 10 years, this is a reminder to hold diversified positions, keep defense and resilience themes on your watchlist, and stay patient when fear starts to dominate the market conversation.

| Entity | Gains | Losses |

|---|---|---|

| Defense contractors | ▲Higher spending outlook | ▼None directly |

| Energy shippers and insurers | ▲Risk premiums rise | ▼Route uncertainty |

| Global exporters | ▲Diversification demand | ▼Supply-chain friction |

| Emerging market stocks | ▲Some strategic tailwinds | ▼Higher volatility |