China Soft Power Gap Shapes Asia Risk Premiums

China and President Xi Jinping are viewed more favorably than the US and Donald Trump across many countries, a shift that matters for trade, capital flows and the balance of power investors price into emerging markets and global supply chains.

The survey points to a widening soft-power gap between Washington and Beijing at a moment when companies, governments and markets are already navigating tariff risk, Taiwan tensions and a more fragmented world order. For investors, that tilt can influence where countries seek investment, whose technology standards they adopt and which side they lean toward in supply-chain and security disputes.

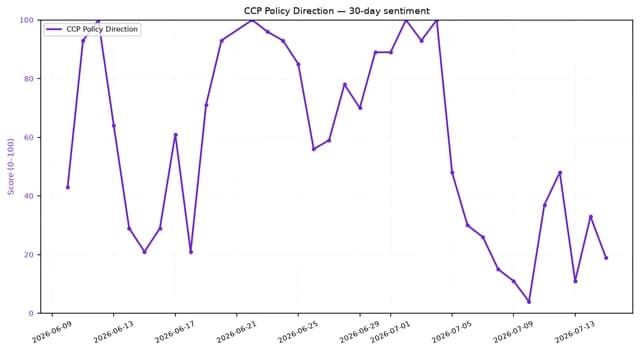

The backdrop is not just diplomatic sentiment. Adalytica’s China CCP Policy Direction Sentiment gauge sits in “Fear” at 19, while its Global Stability Sentiment is in “Extreme Fear” at 7, underscoring how fragile the geopolitical environment has become. The US-China relations sentiment is only neutral at 41, suggesting investors are not pricing in a clean thaw even as public perceptions appear to diverge.

That dynamic is visible in China-focused exchange-traded funds. The iShares MSCI China ETF, FXI, closed at 34.29 on July 15 after trading above 40 earlier this year, while the iShares MSCI Taiwan ETF, EWT, ended at 102.31, still well above its 50-day average but far below its spring highs. The contrasting price action shows investors remain selective: they are willing to buy exposure to Asian growth and supply-chain leverage, but still demand a geopolitical discount where the US-China standoff is most acute.

China’s domestic and external pressures help explain the survey result. Beijing is contending with weaker business confidence, security escalation in the Taiwan Strait, missile testing and broader concerns about economic resilience, even as it continues to project diplomatic and military reach. Washington, meanwhile, is facing skepticism in countries that see US policy as more transactional under Trump-era rhetoric and tariff threats.

For markets, the question is whether favorability translates into policy alignment. If more governments hedge toward Beijing, it could support Chinese trade ties, outbound investment and demand for non-US assets, while complicating US efforts to rally allies around sanctions, export controls and technology restrictions.

The next catalyst is whether the diplomatic calendar narrows or widens the gap, with further US-China tensions, tariff moves and regional security developments likely to keep the investor lens on Asia’s biggest geopolitical fault line.

| Entity | Gains | Losses |

|---|---|---|

| China/Xi | ▲Soft-power standing | ▼US diplomatic influence |

| US/Trump | ▲— | ▼Global favorability |

| FXI / China equities | ▲Selective inflows | ▼Geopolitical discount |

| EWT / Taiwan equities | ▲Supply-chain premium | ▼Taiwan risk premium |