Cooling labor market supports payroll and staffing names

The U.S. labor market is losing steam, and that matters because jobs are the engine of consumer spending, corporate revenues and ultimately stock-market earnings.

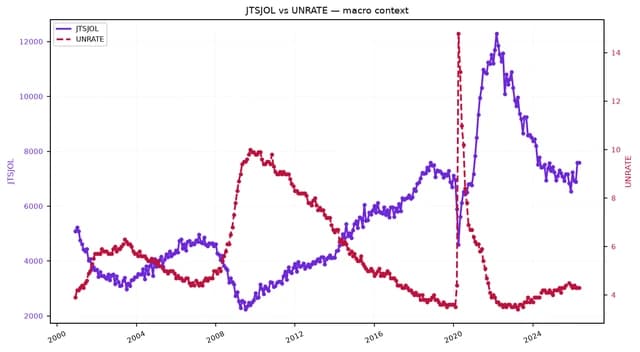

Job openings rose only modestly to 7.6569 million in June from a revised 7.594 million in May, according to the latest data, while the unemployment rate edged down to 4.2% from 4.3%. Nonfarm payrolls reached 158.984 million, still expanding, but the pace is clearly more measured than the post-pandemic hiring boom that once pushed openings above 12 million. For investors, that combination is important: hiring demand is softening, but the economy is not yet flashing outright recession.

That’s the backdrop for payroll processors and staffing firms such as ADP, Paychex and ManpowerGroup. These companies sit close to the heartbeat of employment, so their shares often reflect how employers are thinking before the broader market does. ADP has climbed back above its 50-day moving average and sits well above its 200-day moving average, while Paychex has also rebounded and Manpower has staged a sharp recovery from its spring lows. The moves suggest investors are betting that labor demand may be stabilizing even as companies stay cautious on headcount.

The business case is straightforward. When openings remain elevated, employers still need recruiting, payroll administration, compliance support and flexible staffing solutions. When openings fade, those same companies face slower client growth and less pricing power, even if sticky recurring revenue helps cushion the blow. That’s why firms like ADP and Paychex are often seen as steady compounding businesses in a healthy labor market, while staffing names such as Manpower are more cyclical and can swing with hiring sentiment.

There is also a broader policy and economic angle. A labor market that cools without collapsing gives the Federal Reserve more room to keep inflation on a downward path without forcing a hard landing. A sharp rise in joblessness would be a very different story: it would pressure wages, dent consumer confidence and hit sectors tied to discretionary spending. Current readings point instead to a softer landing narrative, even if the path remains uneven.

Investors should also watch the tension between job cuts and job creation. Big corporate layoffs in manufacturing and technology get headlines, but the aggregate data still show payrolls growing and unemployment near historical norms. That split matters. It means the labor market is being rebalanced rather than destroyed, which is generally healthier for long-term earnings and for companies selling to employers and workers alike.

The next few months will be about whether openings keep drifting lower or settle into a new range. If they stabilize, payroll and staffing firms could continue to recover. If they roll over again, the labor market would move closer to the kind of slowdown that usually reaches consumer spending and stock valuations soon after. For long-term investors, this is a reminder to focus on businesses with durable cash flow and broad customer bases, not just the next payroll print. Worth watching, and for patient investors, worth keeping on the watchlist.

| Entity | Gains | Losses |

|---|---|---|

| ADP, Paychex, Manpower | ▲Steadier hiring demand | ▼Severe labor-market slowdown |

| Employers | ▲More flexibility on headcount | ▼Tighter labor bargaining power |

| Federal Reserve | ▲Easier inflation cooling | ▼Need for emergency easing |

| Consumers | ▲Lower recession risk | ▼Weaker wage growth if hiring cools |