Earnings Season Faces Geopolitical Stress Test

Investors are heading into Q1 earnings season with little room for disappointment as escalating Middle East tensions and a still-fragile macro backdrop keep risk appetite uneven and raise the stakes for company guidance.

That combination matters because earnings are now doing most of the heavy lifting for equity direction. With geopolitical uncertainty pushing up volatility expectations and macro data still being parsed for clues on inflation and policy, markets are likely to reward firms that can defend margins and punish those that show any sign demand is weakening. The result is a tape that can swing sharply on individual results even if the broader index remains near record territory.

The S&P 500 ETF, SPY, has pushed to 754.95 in the latest reading, above its 50-day and 200-day moving averages, but momentum has become more selective. Its RSI reading of 56.7 points to a market that is not overbought, yet not cheap either, while the move higher has come alongside steadily rising volumes. That suggests participation remains solid, but investors are increasingly discriminating about what they own. In technical terms, the index has held its longer-term trend, but the stretch above the 50-day moving average leaves less cushion if earnings or geopolitics disappoint.

Safe-haven demand has not broken out in a decisive way, which implies investors are hedging rather than fully de-risking. TLT, the long-duration Treasury ETF, has been hovering around 84.47, below both its 50-day and 200-day moving averages, indicating bonds are not yet pricing a full-blown growth scare or flight to safety. That leaves equities in an awkward middle ground: vulnerable to bad news, but still supported by the absence of a clear macro shock.

The geopolitical overlay is especially important because it can affect both valuations and fundamentals at the same time. Higher oil prices, supply-chain delays and risk premiums can squeeze consumer discretionary and industrial margins while supporting energy and defense. At the same time, a prolonged uncertainty premium can keep investors from paying up for cyclicals unless earnings visibility improves. For multinational companies, the question is less whether conflict changes demand overnight than whether it alters costs, shipping routes and management commentary for the rest of the year.

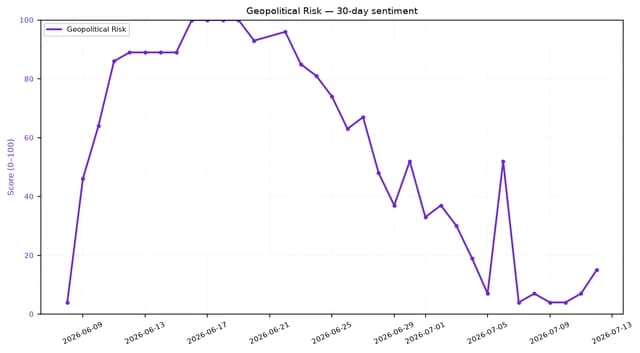

The market’s internal signals also point to caution. Adalytica’s Global Stability Sentiment gauge has dropped to Extreme Fear, even as awareness remains elevated, reflecting a sharp deterioration in perceived geopolitical stability. That gap matters for portfolio positioning: investors may be watching risks closely, but they are still likely to demand a larger margin of safety before adding exposure to sectors most sensitive to trade, energy and supply shocks.

Bullishly, earnings could still validate the market’s resilience. Strong results from technology and financials would support the view that U.S. corporate profit growth remains intact and that companies with pricing power and operating leverage can absorb near-term turbulence. A healthy earnings season could also justify the rally in large-cap equities by showing that valuations are backed by fundamentals, not just liquidity.

The bear case is that geopolitics and a cautious consumer combine to cap upside even where headline earnings look fine. If management teams soften guidance, cite inventory caution or flag margin pressure from freight and input costs, the market’s tolerance for elevated multiples may quickly fade. That risk is most acute in sectors where expectations have already moved ahead of earnings delivery.

For investors, the next catalyst is not just the earnings beat rate but the tone of forward guidance. The market is likely to focus on whether companies can reaffirm margins, capital spending and demand trends in the face of rising uncertainty. Until that is clear, Q1 earnings season looks less like a straightforward reset and more like a test of how much geopolitical risk the market can absorb without revising the growth narrative.

| Entity | Gains | Losses |

|---|---|---|

| Strong earners | ▲Higher multiples | ▼Less tolerance for misses |

| Defensive sectors | ▲Safe-haven bids | ▼Slower upside |

| Energy and defense | ▲Geopolitical tailwinds | ▼Demand volatility |

| Rate-sensitive growth names | ▲Selective support | ▼Guidance risk |