Europe's Rearmament Supports Defense Contractors

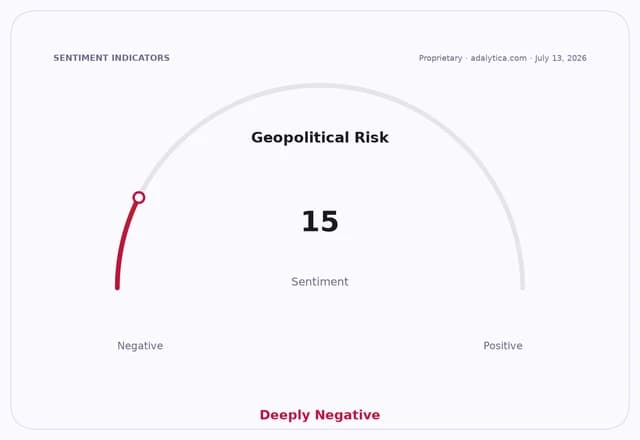

European leaders’ renewed push to keep Ukraine funded is reinforcing one of the clearest investable themes in global markets: defense spending is becoming structural, not cyclical. With global stability sentiment captured by Adalytica.com stuck in “Extreme Fear” even as awareness remains high, the market is still underpricing how persistent Russia-related security risk will keep pressure on governments to buy weapons, replenish stockpiles and harden supply chains.

That matters because Europe’s defense response is no longer about emergency shipments alone. It is moving toward multi-year procurement, industrial capacity expansion and faster military readiness across NATO states. In plain terms, the war has turned defense into a budget priority that competes with welfare spending, yet is increasingly treated as non-discretionary. For investors, that means the revenue visibility for prime contractors and their suppliers is improving even when headlines around cease-fires or diplomacy briefly cool.

The stock action says the trade is alive, but not finished. Lockheed Martin has swung sharply higher this year and now sits just above its 50-day moving average, while Northrop Grumman has also held up better than the broader market despite a rougher stretch in early summer. Boeing, meanwhile, remains far more volatile and still trades well below its recent peaks, showing that not every aerospace and defense name is capturing the same level of policy-driven demand. The message is simple: investors are rewarding the companies most exposed to long-cycle missile, air defense, space and electronics programs, not just those with broad defense branding.

The economic significance is bigger than one budget cycle. Europe’s rearmament requires factories, steel, propulsion, sensors, avionics, cybersecurity and logistics capacity. That creates a second-order capex wave that can spill into smaller suppliers and industrials far beyond the headline contractors. It also helps explain why defense shares have become a refuge when geopolitics deteriorates: governments may delay many forms of spending, but they rarely delay missile defense when the perceived threat is rising.

The market’s mistake is to treat defense as a trade on war headlines. The real opportunity is in the multiyear procurement pipeline that follows them. When EU and Ukraine supporters discuss further aid, they are not just negotiating another funding tranche; they are signaling that Europe’s security architecture is still being rebuilt under duress. That tends to lift order backlogs, extend program visibility and support pricing power for contractors with scarce capacity.

I believe the best way to play this is to stay overweight the defense primes and the picks-and-shovels names tied to munitions, propulsion and battlefield electronics. Lockheed Martin and Northrop Grumman remain the cleanest expressions of the theme, while Boeing offers more of a recovery option than a pure geopolitical hedge. For investors who want broader exposure, defense ETFs can capture the next leg if European aid turns into another wave of procurement.

The takeaway: the EU-Ukraine aid debate is not just a diplomatic story, it is a capital-allocation catalyst. In a world of rising instability, defense spending is becoming a secular megatrend, and the market still has room to reprice the winners.

| Entity | Gains | Losses |

|---|---|---|

| Lockheed Martin | ▲Missile and air-defense demand | ▼Budget-delay risk fades |

| Northrop Grumman | ▲Long-cycle program visibility | ▼Peace-dip traders |

| Boeing | ▲Select defense recoveries | ▼Volatility from mixed portfolio |

| European governments | ▲Stronger deterrence | ▼Higher fiscal burden |