Rising Fuel Prices Pressure Inflation and Transport

Fuel is climbing again, and that matters because it quickly turns into a broader cost shock for households, commuters and small businesses. In places such as Kabul and Pakistan, higher petroleum prices are already forcing public transport operators to raise fares, showing how a move in crude can ripple through the economy far beyond the pump.

That chain reaction is what investors should pay attention to. Transportation is one of the fastest ways energy prices feed into inflation, especially in economies where consumers rely heavily on buses, minibuses and ride-hailing rather than private cars. When fares rise, workers have less money left for food, rent and discretionary spending, while businesses face higher delivery and logistics costs. That can slow demand just as policymakers are trying to keep inflation in check.

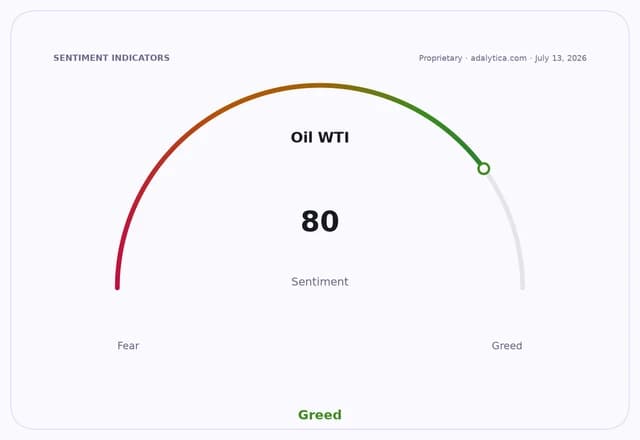

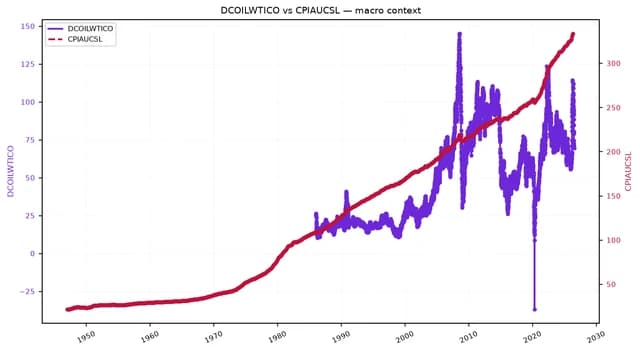

The oil market itself helps explain why the pressure is returning. West Texas Intermediate has rebounded sharply from a recent low near $69 a barrel, and the USO oil fund has reflected that move with a steep run-up over the past few months. Even after a pullback, crude remains high enough to squeeze fuel-dependent sectors. Conventional technical indicators on USO also point to a market that has been volatile rather than calm: the fund’s 50-day moving average has stayed well below recent prices, while RSI readings have swung from deeply overbought to much cooler territory, underscoring how quickly energy sentiment can change.

The inflation backdrop is not friendly either. Consumer prices remain elevated, with headline CPI running far above pre-pandemic levels and core inflation still sticky. That means higher fuel costs arrive on top of an already expensive base, making it harder for households to absorb another round of price increases. In markets like Pakistan, where transport networks are tightly linked to fuel subsidies, any reduction in government support can have an immediate effect on fares and inflation expectations.

For investors, the story cuts both ways. Energy producers and related funds can benefit when crude prices move higher, but transport operators, consumer-facing businesses and import-dependent economies usually feel the pain first. Uber and Lyft may not be the direct victims of a fare hike in South Asia, but the same fuel-driven inflation that raises local bus fares can also pressure consumer spending and ride demand elsewhere if it persists. Over time, sustained fuel inflation tends to favor companies with pricing power and punish those with thin margins and heavy fuel exposure.

The larger narrative is simple: once fuel starts forcing up everyday transport costs, inflation stops looking like a data point and starts looking like a lived experience. That is why markets watch oil so closely. If crude stays firm, public transport fares may be only the first visible sign of a broader squeeze. For long-term investors, this is a reminder to favor diversified portfolios, own businesses that can pass along higher costs, and keep energy volatility on the watchlist rather than dismissing it as noise.

| Entity | Gains | Losses |

|---|---|---|

| Oil producers | ▲Higher revenue | ▼None |

| Public transport operators | ▲None | ▼Higher fuel bills |

| Commuters and households | ▲None | ▼Higher fares, less spending power |

| Inflation-sensitive businesses | ▲Pricing power names | ▼Margin-sensitive firms |