Geopolitical fears hit tech and boost defensives

Wall Street sold off as escalating geopolitical tensions revived demand for safety and knocked the market’s most crowded growth names, with technology stocks leading the decline and the Nasdaq underperforming broader benchmarks.

The move matters because it shows investors still have little margin for error in a market that has leaned heavily on large-cap tech to carry index performance. When risk appetite fades, the sector that has driven much of the market’s upside can also become the main source of downside, especially if tensions threaten supply chains, capital spending and global demand.

The Nasdaq 100 proxy, QQQ, fell to 711.74 on July 13 from 725.51 just three sessions earlier, slipping back below its 50-day moving average of 715.61. The technical picture weakened further as RSI readings dropped to 41.3, suggesting momentum has cooled from the stronger levels seen in late June. The XLK technology ETF also slid to 181.28 from 185.78 on July 10, leaving it just above its 50-day moving average of 181.32 and well below its recent peak. By contrast, the S&P 500 proxy SPY held up better at 749.17, underscoring that the selling was concentrated in growth and technology rather than a full-blown market panic.

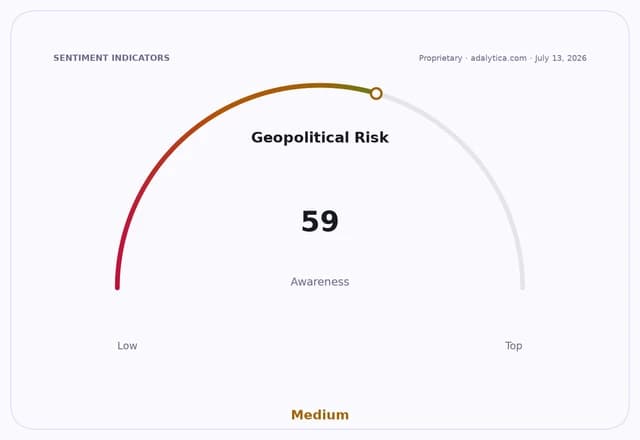

That relative resilience does not mean the market is untroubled. Adalytica’s Global Stability Sentiment gauge has plunged to 15, labeled “Extreme Fear,” from 52 a week earlier, while its awareness reading remains elevated. The shift aligns with the broader pattern in U.S. rates and equities: the 10-year Treasury yield, at 4.58% in the latest reading, has stayed high enough to keep valuation pressure on long-duration assets, while geopolitical risk adds another layer of uncertainty for earnings and capital allocation.

For technology companies, the transmission mechanism is straightforward. The sector is highly exposed to cross-border trade, semiconductors, hardware supply chains and international demand, and companies such as Microsoft and Apple have already flagged geopolitical tension, tariffs and conflict as business risks in recent filings. That makes tech vulnerable not only to direct disruption, but also to investor de-risking when the geopolitical backdrop deteriorates.

The bear case is that tensions keep widening and force a more defensive market rotation, leaving richly valued megacap tech to lag until visibility improves. The bull case is that any dip remains a buying opportunity so long as the geopolitical shock does not translate into a material earnings downgrade or a broader economic slowdown. With the U.S. recession indicator still flat at zero, investors are treating the episode as a risk-event rather than a recession signal for now.

What to watch next is whether the selloff spreads beyond tech into cyclicals and financials, and whether Treasury yields or crude react in a way that would make the market repricing more durable. If tensions persist, technology could remain the first place investors trim exposure and the last sector to recover once the fear premium fades.

| Entity | Gains | Losses |

|---|---|---|

| Treasury bonds | ▲Safe-haven demand | ▼Equity risk appetite |

| Defensive sectors | ▲Relative inflows | ▼Tech leadership |

| Tech megacaps | ▲Long-term franchise demand | ▼Near-term valuation support |

| Exporters/importers | ▲— | ▼Supply-chain visibility |