Geopolitical Yield Surge Hurts Duration

European bond yields are climbing again, but the market is not pricing a fresh inflation breakout so much as a global repricing of duration driven by geopolitics, higher energy risk and a synchronized selloff in sovereign debt.

That distinction matters. If yields were rising because growth and inflation were accelerating in Europe, the trade would favor cyclical equities, banks and shorter-dated credit less dramatically. But when yields rise for exogenous reasons — a jump in oil prices, Middle East tension and a broader move higher in U.S. and Japanese government bond yields — the message to investors is different: financing costs are being re-marked higher even without a cleaner growth story behind them.

The U.S. 10-year Treasury yield has pushed to 4.56%, while the federal funds rate sits at 3.63% and the yield curve has steepened modestly, with the 10-year minus 2-year spread at 0.42 percentage point. That is not the signature of an inflation panic alone; it is a market recalibrating the term premium and demanding more compensation for holding long-dated government debt in an unstable geopolitical backdrop. European bonds are being pulled into that global move.

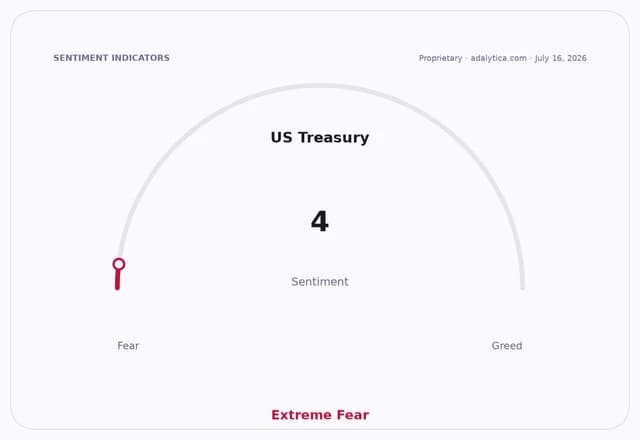

The bond market reaction is already visible in ETFs that track duration. The iShares 7-10 Year Treasury Bond ETF, IEI, is hovering around 116.86, essentially flat to slightly below its 50-day moving average of 116.81 and its 200-day average of 117.09, while its RSI has faded to 43.6. That says momentum is weak, not broken, but the market is no longer rewarding duration exposure. The iShares 20+ Year Treasury Bond ETF, TLT, has been hit harder: it closed at 83.94, below both its 50-day average of 84.95 and its 200-day average of 86.03, with an RSI of just 12.2. In Adalytica.com’s U.S. Treasury Bonds Trade Signals, TLT is flashing “Extreme Fear,” with sentiment at 4.0 and a 7-day drop of 67%. That is the kind of positioning washout that can occur when investors suddenly decide longer bonds are the wrong place to hide.

For Europe, the economic implications are immediate. Higher sovereign yields raise the benchmark cost of capital for governments, corporates and households just as policy makers were hoping to preserve some room for growth. That matters most for highly indebted euro-zone issuers, leveraged sectors and rate-sensitive assets such as real estate and utilities. It also tightens financial conditions even if the European Central Bank is not the direct catalyst.

For investors, the market is telegraphing a shift away from pure duration and toward assets that benefit from higher nominal rates, resilient cash flow and pricing power. Shorter-duration bond funds, floating-rate credit and select financials are better placed than long-duration sovereign proxies if the move in yields is being driven by supply, geopolitics and global term-premium re-pricing rather than a clean European growth upswing.

The deeper narrative is that bond markets are losing their old safe-haven symmetry. When U.S., Japanese and European yields rise together, investors can no longer rely on sovereign debt as a universal shock absorber. That is bullish for inflation hedges, commodity-linked sectors and balance-sheet-light businesses that can pass through costs. It is bearish for duration, for countries with heavy refinancing needs and for any equity story that depends on cheap money staying cheap.

If this move persists, the next winners are likely to be the market’s usual second-order beneficiaries: energy, defense, select banks and infrastructure plays with pricing power. The losers are long-duration bonds, rate-sensitive property assets and issuers that need to refinance into a more expensive world. For investors, the takeaway is simple: this is not just an inflation trade, it is a geopolitical re-pricing of capital — and that creates one of the clearest rotation opportunities of the year.

| Entity | Gains | Losses |

|---|---|---|

| Energy stocks | ▲Higher oil-linked pricing | ▼Bond bulls |

| Banks | ▲Wider rate spreads | ▼Duration-heavy portfolios |

| Long-duration Treasuries | ▲— | ▼Term-premium repricing |

| Rate-sensitive property/utility names | ▲— | ▼Higher financing costs |