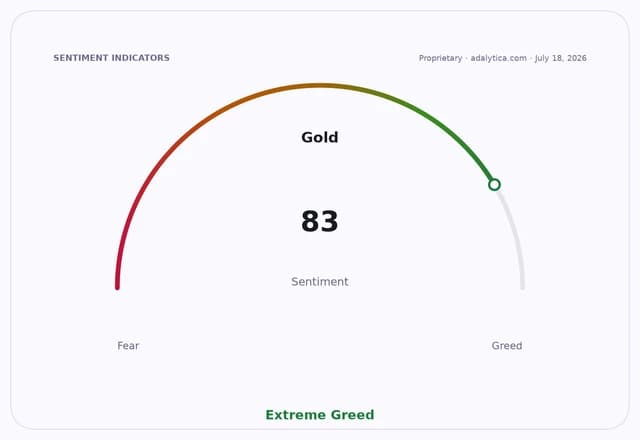

Gold Consolidation Hints at Next Macro Breakout

Gold is still trading like a macro hedge, but the market is underestimating how quickly that can turn into another leg higher if real yields soften again and geopolitical stress stays elevated.

For investors asking “how much is 21 karat now?” the answer is increasingly less about a simple retail quote and more about a global price regime that remains extraordinarily sensitive to the U.S. Treasury market, central-bank policy and safe-haven flows. The 10-year Treasury yield is sitting near 4.56%, far above the emergency-era lows that powered gold’s last major breakouts, yet bullion has held unusually firm after a violent spring selloff. That combination tells you gold is not being priced as a speculative momentum trade anymore; it is being treated as strategic insurance.

That matters because the gold market is doing two things at once. First, it is signaling that investors still want protection against inflation surprises, fiscal slippage and geopolitical shocks. Second, it is exposing a disconnect between paper gold and the jewelry market. In Thailand, domestic gold prices have risen, with SJC gold jewelry recently quoted around 64,900 baht, while weaker demand has pressured some gold ring brands. That split is exactly the kind of divergence that tends to show up when investment demand, not consumer buying, is driving the tape.

The ETF data reinforces that view. SPDR Gold Shares has been volatile, but it is still far above its longer-term trend and has spent much of the year in stretched technical territory. Technical readings such as the 50-day moving average, RSI and MACD show a market that has cooled from extreme overbought levels but has not broken structurally. In plain English: gold is consolidating, not collapsing. That is usually what happens before the next macro catalyst.

Mining shares are telling a more interesting story. The VanEck Gold Miners ETF has been far more volatile than bullion, and that is where the asymmetric setup lies. When gold trends higher, miners tend to expand margins quickly because their costs lag the metal. When gold stalls, the stocks get punished first. That creates opportunity for investors who can tolerate volatility and focus on quality producers, royalty names and low-cost operators. If the macro backdrop turns more favorable, miners can outperform bullion by a wide margin.

Silver is also flashing a different kind of opportunity. The iShares Silver Trust has been crushed from its highs, even as industrial demand and monetary demand can both benefit in a reflationary or risk-off surge. That makes silver a classic second-order trade: it is not just a precious metal, but a leveraged call on both gold sentiment and industrial recovery.

The larger narrative is simple. The market is not pricing gold as a one-way rocket ship; it is pricing it as a contested but durable store of value in a world of sticky yields, geopolitical uncertainty and uneven consumer demand. That is exactly the kind of backdrop that favors accumulation on weakness, not chase-the-panic buying. If you want exposure, the cleaner trade is not physical jewelry at retail markups, but liquid vehicles tied to bullion and select miners with operating leverage.

My thesis: the market underestimates how resilient gold can be if real rates roll over even modestly from here. That makes the current consolidation an inflection point, not a warning sign. For investors, the best way to play it is through gold bullion ETFs, high-quality gold miners and, for more aggressive upside, silver as a beta trade on the same macro thesis.

| Entity | Gains | Losses |

|---|---|---|

| Gold bullion holders | ▲Safe-haven protection | ▼Opportunity cost if yields rise |

| Gold miners | ▲Margin leverage on higher gold | ▼Cost pressure if gold stalls |

| Jewelry retailers | ▲Inventory repricing power | ▼Weak consumer demand |

| Treasury bear market / higher real yields | ▲Attractive income appeal | ▼Gold upside narrative |