Hawkish Fed Risk Boosts Energy, Pressures Growth

Markets are entering Kevin Warsh’s two days of testimony in no mood for reassurance: Asian equities are sliding, Brent is holding near $85 a barrel, and US rates remain pinned close to levels that already feel restrictive for growth. The combination raises the risk that the Fed leans hawkish just as geopolitical stress in the Middle East keeps energy inflation alive, a setup that could keep borrowing costs elevated and prolong the pressure on global risk assets.

That matters because the macro mix is turning more hostile for the two engines that have carried markets: easier money and cheap oil. The US 10-year Treasury yield is around 4.59%, while the 2-year is near 4.25%, a curve that says policy is still tight and that markets are not pricing an easy path to cuts. Fed funds, meanwhile, are forecast around 3.63%, showing officials still have room to defend a restrictive stance if inflation re-accelerates.

The problem for investors is that energy is reasserting itself as a tax on the rest of the market. Brent’s hold near $85 a barrel, along with USO and BNO both trading far above their longer-term averages, tells you crude traders are pricing more than a passing supply scare. USO’s close around 120 is still well above its 200-day moving average near 97, while BNO sits near 47 versus a 200-day average under 39. Those are not the kind of charts that signal complacency.

This is where the market may be underestimating second-order effects. A hawkish Fed, even if only rhetorically hawkish, pushes up the discount rate on every growth story. At the same time, higher oil prices feed through to transportation, chemicals, airlines, industrials and consumer spending. That is a bad backdrop for Asian equities already wobbling before the hearings, because export-heavy and rate-sensitive markets get hit from both sides: tighter global financial conditions and a more expensive energy bill.

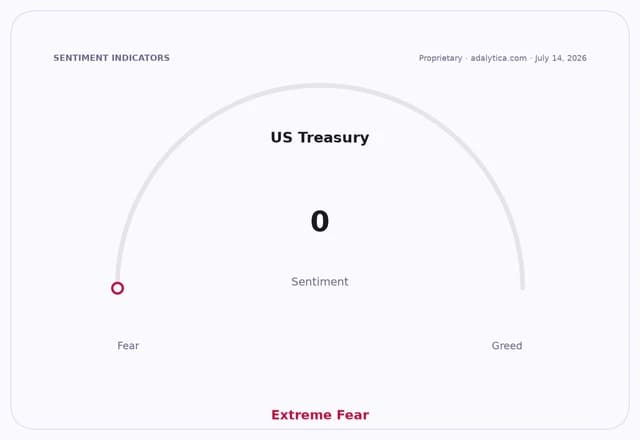

The bond market is flashing the same caution. Adalytica’s US Treasury Bonds signal sits at “Extreme Fear,” while its Global Stability reading is also in “Extreme Fear,” even as the awareness gauge is elevated. In plain English, investors know the risk is rising, but positioning still looks defensive rather than panicked. That is often the zone where moves extend, not reverse.

For investors, the opportunity is not to chase the broad market dip but to own the beneficiaries of scarcity, volatility and capital discipline. Energy producers with strong balance sheets, oilfield services, and infrastructure names with pricing power should outperform if crude stays bid and the Fed keeps policy tight. Chevron and ConocoPhillips have already warned in filings that commodity prices and geopolitical disruption are core drivers of profitability, and that is exactly the type of environment that rewards upstream cash generation. Defense and select logistics names can also benefit if Middle East risk keeps premium embedded in commodities and freight.

The market’s bigger mistake is assuming this is just another headline risk for crude. It is not. A hawkish central bank in the face of geopolitical tension creates a regime where inflation is harder to kill, multiples are harder to expand, and capital naturally rotates toward real assets and toll-road businesses rather than long-duration growth. If Warsh reinforces that message in Congress, this could be an inflection point for positioning, not a footnote.

The takeaway is simple: stay long the upstream energy complex, the infrastructure tied to secure supply, and the defense/volatility trade, while treating rate-sensitive and energy-intensive equities as the vulnerable side of the ledger until the Fed proves it can talk tough without breaking growth.

| Entity | Gains | Losses |

|---|---|---|

| Energy producers | ▲Higher crude prices | ▼Margin pressure from volatility easing |

| Oilfield services | ▲Stronger upstream spending | ▼Slower capex if prices retreat |

| Rate-sensitive equities | ▲— | ▼Higher discount rates, tighter policy |

| Oil importers / Asian equities | ▲— | ▼Costlier energy, weaker risk appetite |