Housing slowdown pressures real estate commissions

Homebuyers are confronting a market that is still expensive, still thin on supply and increasingly contentious over what real estate agents earn for a sale.

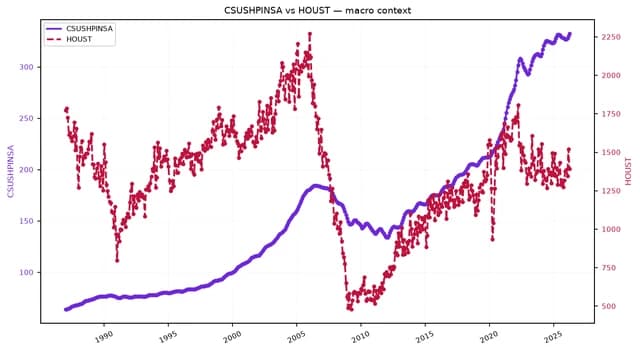

That matters because commissions sit at the center of how homes are bought and sold in the U.S., and the latest housing data show a market where pricing remains elevated even as activity softens. The S&P CoreLogic Case-Shiller home price index rose to 332.678 in April, up 0.77% from March and near a forecast 333.2757 in May, underscoring that affordability remains strained despite a cooler pace than the pandemic-era surge.

At the same time, new housing supply is weakening. U.S. housing starts fell to 1.177 million in May from 1.392 million in April, a 15.45% drop, while the unemployment rate held near 4.2% in June. For agents and brokers, that combination means fewer transactions, more negotiation pressure and less room to justify traditional 3% commissions on both sides of a deal.

The brokerage and portal industry is already under stress. Zillow shares trade at $32.19, far below the 50-day average of $35.61 and the 200-day average of $54.59, after a sharp slide from the high-80s last year. CBRE, a broader real estate services bellwether, has also given back ground, closing at $138.03 versus a 200-day average of $148.92, even after a rebound from February lows.

Investors are watching whether the commission model can hold as buyers and sellers become more price-sensitive and as competition increases from discount brokers, listing platforms and agents offering lower-fee services. If fewer homes are being started and sold, the fight over who gets paid what on each transaction becomes more important to brokerage revenue, portal monetization and agent economics.

The bigger narrative is that U.S. housing remains locked in a low-volume, high-price pattern: sellers still have pricing power in many markets, but transaction counts are soft enough to pressure everyone in the value chain. The next catalyst is the trajectory of mortgage rates, which will determine whether tighter affordability continues to squeeze sales and intensify scrutiny over the standard 3% commission.

| Entity | Gains | Losses |

|---|---|---|

| Homebuyers | ▲Lower-fee options | ▼Traditional commission burden |

| Discount brokerages | ▲Share gains | ▼Full-service agents |

| Zillow and portals | ▲Traffic from fee debate | ▼Weaker housing turnover |

| Traditional realtors | ▲High-fee model | ▼Margin pressure from slower sales |