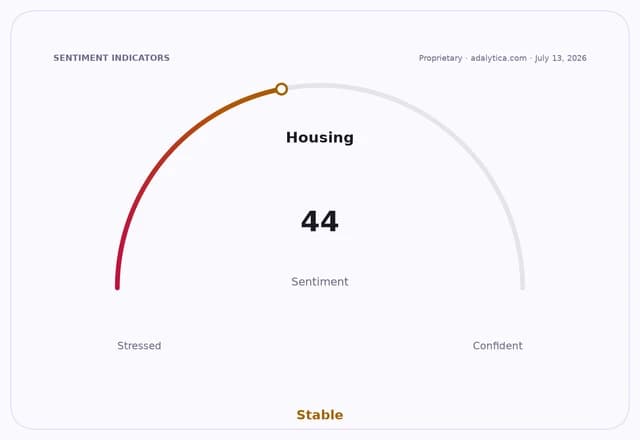

Housing Slump Tied to Affordability, Not Demand

Mortgage rates near 4.5% are doing the most damage to U.S. housing activity, and Zillow’s latest read on the market suggests the slump in sales is being driven less by a collapse in buyer interest than by the affordability squeeze keeping owners and would-be movers on the sidelines.

That distinction matters because it points to a housing market that is constrained, not broken. Sales can remain weak even when underlying demand exists if financing costs keep monthly payments out of reach. The 10-year Treasury yield, a key benchmark for mortgage pricing, has climbed to around 4.55%, while the labor market is still comparatively healthy, with unemployment at 4.2% and forecast to edge only slightly lower. In other words, households have jobs, but borrowing costs remain high enough to freeze turnover.

The result is a market where prices have stayed elevated relative to incomes, even as transactions remain sluggish. Housing activity is now being shaped by the gap between what buyers can afford and what sellers are willing to accept. When rates stay high, homeowners with cheaper existing mortgages are also less inclined to list, further tightening supply and muting the number of deals that can actually clear.

For investors, that has a direct read-through to the housing ecosystem. Zillow Group and sister platform Zillow, or Z, has seen its shares fall sharply from levels above $80 last year to about $32, reflecting concern that a prolonged affordability downturn will keep the residential resale market thin. Rival Zillow Group Inc. shares, ZG, have followed a similar path, underscoring how little relief the sector has received from intermittent hopes of rate cuts. Technical readings on both stocks remain weak, with prices below their 200-day moving averages and momentum indicators still below earlier peaks, a sign the market remains skeptical that a quick rebound in housing turnover is imminent.

The macro backdrop helps explain why. The Fed’s policy easing cycle has not translated into materially cheaper long-term borrowing costs, and the bond market is still pricing a fairly restrictive financing environment. Adalytica’s Treasury trade signal is in “fear,” reflecting investor caution around duration exposure, while its Housing and Rent Inflation Sentiment gauge is neutral, suggesting the debate is still centered on whether housing costs will ease meaningfully or merely plateau at a high level.

That leaves Zillow in a tricky but potentially constructive position. A weak resale market can still support traffic on listing portals as consumers search, compare and wait for better conditions. But for monetization to improve, the company ultimately needs transaction volumes to recover, not just engagement. Zillow Home Loans has shown growth in purchase originations, according to recent filings, but that business still depends on a healthier housing market to scale.

The bull case is that rates eventually drift lower, pent-up demand returns, and sales volumes snap back because many households have delayed moves for years. The bear case is that affordability remains stretched long enough to normalize lower turnover as the new baseline, leaving prices sticky but activity subdued. For now, Zillow’s message is that the market is not short on interest — it is short on affordability.

| Entity | Gains | Losses |

|---|---|---|

| Home sellers with low-rate mortgages | ▲Higher price support | ▼Fewer buyers able to transact |

| First-time buyers | ▲Possible eventual rate relief | ▼Current affordability squeeze |

| Zillow and Zillow Group | ▲More search traffic | ▼Weak resale volumes |

| Mortgage lenders | ▲Refinance and purchase demand if rates ease | ▼Thin origination pipeline if rates stay high |