Iran Risk Fuels Oil and Defense Trades

The biggest economic story isn’t just that Washington has acknowledged a war with Iran would blow up its China strategy. It’s that the Middle East is now colliding with the U.S.-China contest in a way that can jolt energy, shipping and industrial supply chains at the same time, and investors are starting to price that risk into oil-linked assets.

That matters because the U.S. can’t afford a prolonged Iran conflict if its broader goal is to contain Beijing, preserve Asian trade flows and keep inflation from reaccelerating. A war would strain naval assets, raise the cost of securing chokepoints and threaten the very energy routes that keep China’s factories and global manufacturing running. In other words, the geopolitical premium is no longer an abstract headline risk; it is a direct tax on the world’s two most important growth engines.

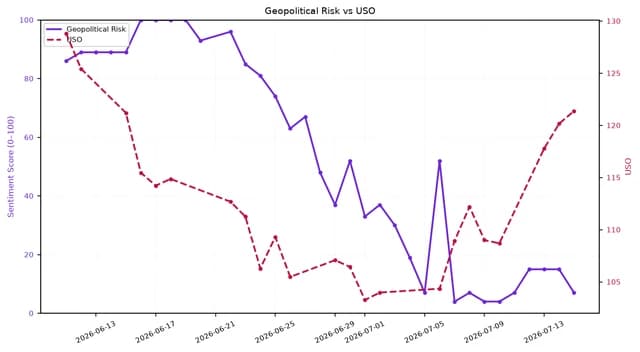

The market is already signaling that stress. USO, the oil ETF, has surged to 121.38 from 106.29 in late June, a move that has lifted it far above its 50-day moving average and pushed its 14-day RSI to 70.2, a conventional technical indicator that suggests momentum is stretched. XLE, the energy sector ETF, has also climbed, though less explosively, to 56.50, while holding near its 50-day moving average. That combination says traders are not only betting on higher crude, they are also looking for cash flow leverage across the integrated majors, producers and service names that benefit from any sustained risk premium.

The deeper point is that oil is acting as the first-order barometer of a much larger strategic shock. If conflict with Iran threatens shipping lanes, insurance costs and regional infrastructure, then China becomes the principal economic casualty: higher import bills, weaker industrial margins and more pressure on already fragile domestic growth. Beijing’s dependence on energy imports means it absorbs the inflation first, while the United States exports the instability. That is why this is more than a foreign-policy warning; it is a supply-side macro event with global inflation implications.

Investors should also pay attention to cross-asset positioning. Global stability sentiment, as tracked by Adalytica.com, has plunged to “Extreme Fear,” while U.S.-China relations sentiment has slipped back toward neutral after recent whipsaws. That tells you the market is not treating this as a contained Middle East flare-up. It is pricing a broader regime shift: more defense spending, more energy security capex, more reshoring and more demand for the infrastructure that makes supply chains resilient.

The winners in this setup are the obvious but still underappreciated ones: oil producers, integrated energy companies, LNG infrastructure, shipping and defense contractors. The losers are airlines, refiners with no upstream hedge, industrials dependent on cheap energy, and import-heavy Asian manufacturers, especially in China, where any jump in feedstock and freight costs hits margins fast. Helium export restrictions tied to the tensions are a reminder that the shock can spread beyond crude into specialized industrial inputs that matter to semiconductors, manufacturing and medical technology.

My view is that the market underestimates how persistent this premium can become. Once the U.S. publicly concedes that war with Iran would wreck its China posture, the strategic incentive is to deter escalation, not absorb it. That usually means a longer period of uncertainty, not a quick resolution. For investors, the asymmetric play is to stay long energy and defense exposure on weakness, and to treat any pullback in oil-linked names as a chance to buy the geopolitical hedge before consensus catches up.

| Entity | Gains | Losses |

|---|---|---|

| USO / oil bulls | ▲Higher crude premium | ▼Demand destruction risk |

| XLE / energy producers | ▲Cash flow leverage | ▼Volatility from policy shocks |

| China / importers | ▲None | ▼Higher energy and freight costs |

| Defense / security names | ▲More spending urgency | ▼No meaningful downside from calm |