Laos Prioritizes Inflation Control Amid Kip Pressure

Laos is stepping up efforts to keep inflation contained as authorities try to protect a fragile recovery from renewed price pressure, a weakening currency and tighter financial conditions.

The government has ordered ministries, branches and localities to improve forecasting and prepare response scenarios, underscoring that price stability has become the central policy priority. That matters because Laos has only recently posted its strongest GDP growth in more than two decades, and policymakers are trying to avoid a repeat of the inflation and exchange-rate stress that eroded household purchasing power and business confidence in recent years.

Official data suggest the challenge is manageable for now but far from resolved. The consumer price index is projected to rise to 336.06 in June from 333.98 in May, implying a monthly increase of about 0.62%, while core inflation is seen climbing 0.25% to 336.97. Those are not crisis readings, but they reinforce the case for vigilance after prices accelerated sharply earlier in the year. The broader CPI series has risen more than 29% from the March level cited in the data, while the core measure is up nearly 26% over the same period, evidence that underlying inflationary pressure has not fully eased.

The policy response is aimed at preventing a price spike from becoming a broader macroeconomic problem. Laos has limited room for error: a large trade deficit keeps pressure on the kip, and imported goods remain a major channel for inflation. When the currency weakens, the cost of fuel, food and industrial inputs rises quickly, feeding through to consumers and squeezing margins for local businesses. That makes forecasting, reserve management and flexible interest-rate policy economically important, not just bureaucratic housekeeping.

Market signals show investors are already factoring in that fragility. Ten-year U.S. Treasury yields have been edging up, but the more relevant local backdrop is the pressure on risk assets tied to inflation expectations and dollar strength. Gold has retreated from its recent highs, while the U.S. dollar has weakened on the Adalytica trade-signal gauge, suggesting global markets are not pricing a broad inflation scare — yet Laos remains exposed to imported price shocks if local policy slips or foreign exchange buffers prove inadequate.

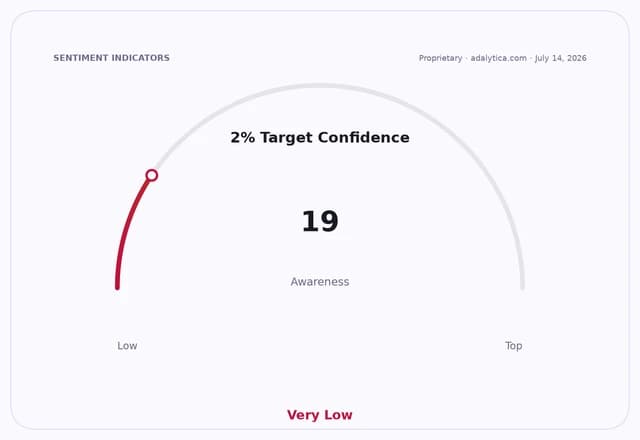

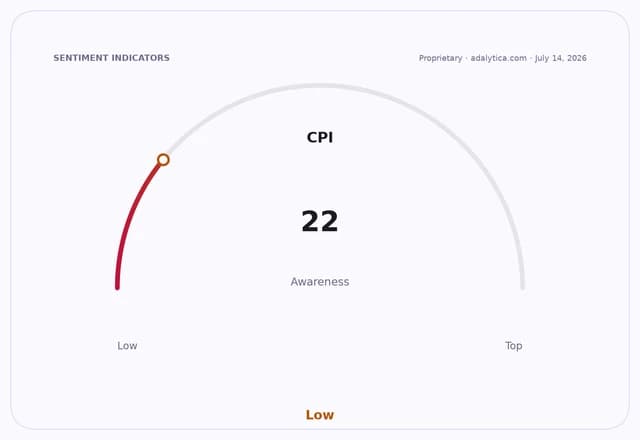

Adalytica’s CPI sentiment reading is at 14, or “Extreme Fear,” while confidence in the Fed’s 2% inflation target sits even lower at 7, also “Extreme Fear.” Those proprietary gauges are not official policy indicators, but they capture how quickly inflation anxiety can return when price data turn higher and policy credibility is questioned. For Laos, the risk is less about U.S. inflation dynamics and more about whether domestic authorities can maintain enough confidence in the kip and enough supply stability to prevent pass-through from turning temporary pressure into persistent inflation.

For investors, the message is that Laos is prioritizing macro stability over growth at the margin. That may help preserve the gains in GDP, but it also suggests tighter liquidity, more caution on credit expansion and continued sensitivity in the banking system. The bullish case is that early intervention, reserve accumulation and a steadier currency can cap inflation before it spreads. The bearish case is that the underlying vulnerabilities — external deficits, imported inflation and credit quality concerns — overwhelm policy tools if global conditions turn less favorable.

What happens next will hinge on whether June and July price data confirm a cooling trend or force more aggressive action on rates, reserves and price controls. If inflation stays near current levels, authorities may preserve growth momentum. If it accelerates, the trade-off between stability and expansion will become sharper, and investors will reassess the durability of Laos’s recovery.

| Entity | Gains | Losses |

|---|---|---|

| Lao government | ▲Policy credibility | ▼Room for growth-first easing |

| Consumers | ▲Price stability if measures work | ▼Purchasing power if inflation rises |

| Banks and lenders | ▲Lower systemic stress if kip stabilizes | ▼Credit demand if conditions tighten |

| Importers | ▲More predictable costs | ▼Margins if currency weakens |