Leisure Travel Revenue Tops Pre-Pandemic Levels

Hotel leisure travel revenue is set to top pre-pandemic levels this year, underscoring how firmly U.S. travelers have shifted back toward discretionary spending even as confidence wobbles and the broader economic backdrop remains uneven.

The significance is not just that rooms are filling again, but that pricing power has held. Marriott and Hilton have been able to push average rates higher while leisure demand stays resilient, allowing hotel revenue to recover faster than the broader economy in real terms. That matters because hotel room revenue is a clean read on the consumer’s willingness to spend on experiences, and it suggests travel remains one of the last areas where households are still absorbing higher prices without a material pullback.

Hilton’s first-quarter filing said strong leisure transient demand drove comparable hotel RevPAR up 4.4% year on year and guided to full-year RevPAR growth of 3% to 4.5%. Marriott has also pointed to solid transient demand and improving group business. Those forecasts imply the industry is not merely rebounding from the pandemic collapse; it is moving into a higher revenue base than 2019, helped by rate increases as well as occupancy gains. In other words, the recovery is being powered by both volume and yield.

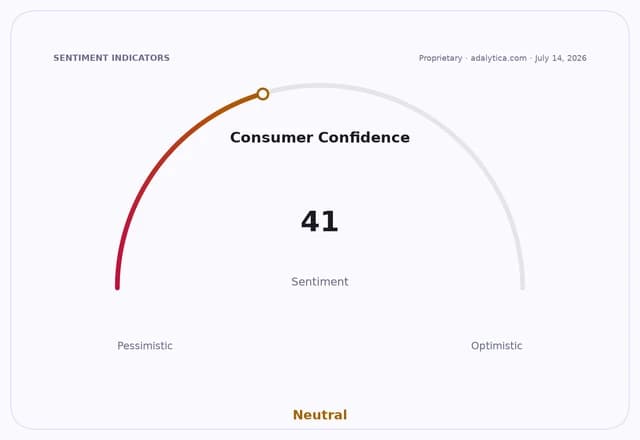

That makes the sector economically important well beyond hotels themselves. Higher leisure travel revenue supports airlines, online travel agencies, cruise operators and a wide swath of consumer-facing service businesses. The latest industry signals also suggest the spending rotation away from goods toward services is still intact, even as consumer sentiment indicators remain mixed. Adalytica’s Consumer Spending Sentiment gauge is flashing extreme greed, while its recession-confidence measure is neutral but volatile, a combination that points to strong near-term spending appetite but little clarity on how durable it will be if the macro picture deteriorates.

For investors, that creates a familiar split. Hotel owners and operators benefit from resilient rates, but the bull case is more complicated than simply “revenues up.” If leisure demand remains strong, Marriott, Hilton and peers can continue to expand fees and margins. If it softens, the downside can come quickly because hotel demand is cyclical and pricing can normalize fast. Hilton shares have held above both their 50-day and 200-day moving averages, while Marriott’s recent trading has been more volatile but still above longer-term trend levels, suggesting markets are still giving the sector credit for earnings durability.

The bear case is that the current strength may be masking consumer strain. Travel is discretionary, and a cooling labor market, tighter credit conditions or a broader slowdown could pressure booking windows and rate growth later this year. That risk is particularly relevant after years of pent-up demand have already been spent down. But for now, the message from hotel revenue, RevPAR guidance and the latest equity action is clear: leisure travel has not merely normalized, it has become one of the clearest beneficiaries of households continuing to trade down in some categories while still trading up in experiences.

The next test is whether this revenue resilience can survive the second half of the year, when rate growth is expected to moderate. If it does, hotel stocks should continue to be treated less like pure reopening plays and more like cash-generative consumer compounders. If it does not, the sector’s premium to 2019 will look more fragile than the headline suggests.

| Entity | Gains | Losses |

|---|---|---|

| Hotel operators | ▲Higher room revenue | ▼Rate-growth pressure later |

| Leisure travelers | ▲More travel options | ▼Paying higher prices |

| Hotel investors | ▲Stronger cash flow | ▼Cyclical downside risk |

| Consumer staples/goods | ▲Less spending share | ▼Services/travel gain share |