Nvidia Rallies Face Slower Multiple Expansion

Nvidia’s stock still has the ingredients to mint big gains for patient investors, but the easy money from the AI trade is getting harder to count on as the chip cycle matures and Treasury yields stay elevated.

The case for Nvidia remains rooted in one dominant fact: demand for AI accelerators is still running ahead of supply. That broader backdrop is keeping the semiconductor complex hot, with Intel raising server-chip prices, Samsung forecasting record quarterly operating profit from AI demand, and memory-chip makers benefiting from a global upcycle that is drawing in fresh capital.

For Nvidia holders, that matters because the company sits at the center of the AI build-out. The stock closed at $210.96 on July 10, above its 200-day moving average of $191.47 and roughly even with its 50-day average of $209.07, a sign the market still treats it as a core AI winner even after a powerful run. But momentum has cooled: the shares have slipped from a 2026 peak of $235.47 in mid-May, and the RSI at 50.3 shows neither overbought nor deeply oversold conditions.

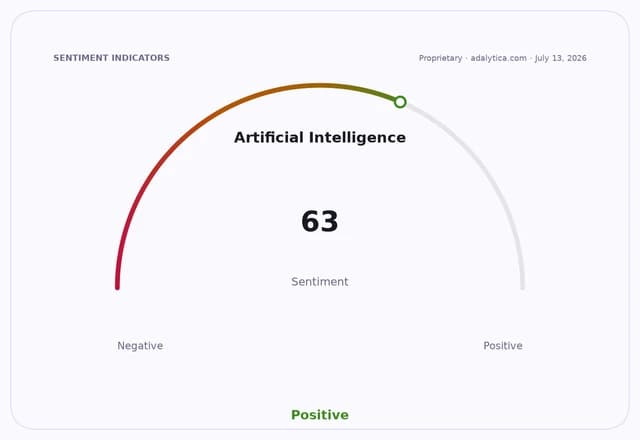

The market is also signaling a more selective phase for AI exposure. Adalytica’s NVIDIA Earnings Sentiment snapshot shows sentiment at 22, labeled “Fear,” even as awareness sits at 81, or “Greed,” suggesting investors are highly focused on the name but less convinced near-term upside will repeat the first leg of the rally. The broader AI gauge is more constructive, with neutral sentiment at 63, but that reflects an industry still rich in opportunity rather than a guarantee that one stock will dominate returns indefinitely.

That is where the millionaire question becomes more realistic than rhetorical. Nvidia can still compound at a rate that rewards long-term holders if AI infrastructure spending keeps climbing and margins hold, but the bar for another multiyear surge is higher now. The stock is already enormous, the sector is crowded, and rivals including AMD and Taiwan Semiconductor Manufacturing are also capturing investor attention as the market looks for second-order beneficiaries of the AI build-out.

Rising rates add another layer of pressure. The 10-year Treasury yield was 4.55% on July 7 and remained near 4.54% to 4.56% this week, a level that makes high-growth valuations more sensitive to earnings execution and guidance. That does not break the Nvidia story, but it does mean investors are paying more for certainty and less for hype.

The broader economic signal is still supportive: U.S. industrial production is forecast to rise to 103.0536 in June from 102.6475 in May, and factory activity tied to semiconductors remains a key beneficiary of AI spending. For Nvidia, the next test is whether demand from cloud giants and enterprise buyers can keep outpacing supply as competitors, customers and new in-house chip efforts all try to carve out share.

The stock can still make long-term investors rich, but the path is now likely to be earned through execution rather than multiple expansion alone.

| Entity | Gains | Losses |

|---|---|---|

| Nvidia longs | ▲AI-led compounding | ▼Slower multiple expansion |

| Nvidia shorts | ▲Near-term valuation reset | ▼Continued AI demand strength |

| AMD and TSMC | ▲Second-order AI exposure | ▼Nvidia market share dominance |

| AI infrastructure buyers | ▲More supply over time | ▼Higher chip and capex costs |