SBI Bets on Southeast Asia Crypto Infrastructure

SBI Holdings’ move to take a majority stake in Coinhako is more than a regional expansion: it is a bet that Southeast Asia will be one of the next battlegrounds for regulated crypto trading and payments infrastructure.

The deal gives the Japanese financial group a firmer operating base in a market where retail adoption, cross-border flows and digital-asset use cases are still expanding, even as global crypto volatility remains high. For SBI, which has long treated digital assets as a strategic growth area, the transaction offers a way to pair balance-sheet strength and institutional reach with local distribution in Singapore and the wider ASEAN corridor.

That matters economically because Southeast Asia remains one of the world’s most attractive growth pools for financial technology. A larger presence there could help SBI capture trading volumes, custody fees and future brokerage or settlement revenue tied to tokenised assets and payments. It also signals that major traditional finance players are still willing to allocate capital to crypto infrastructure despite repeated boom-bust cycles in the asset class.

For investors, the logic is two-sided. On the bullish case, SBI is diversifying away from slower-growing domestic financial businesses and positioning itself for a longer-duration digital-asset cycle. A regulated platform in Singapore can be valuable if the region continues to tighten oversight while supporting legitimate crypto activity, creating a moat for operators with licences, compliance systems and banking relationships. On the bearish side, the purchase is still exposed to the same risks that have dogged the sector: low fee visibility, sharp swings in crypto trading activity, regulatory shifts and the possibility that investor enthusiasm cools before the business scales.

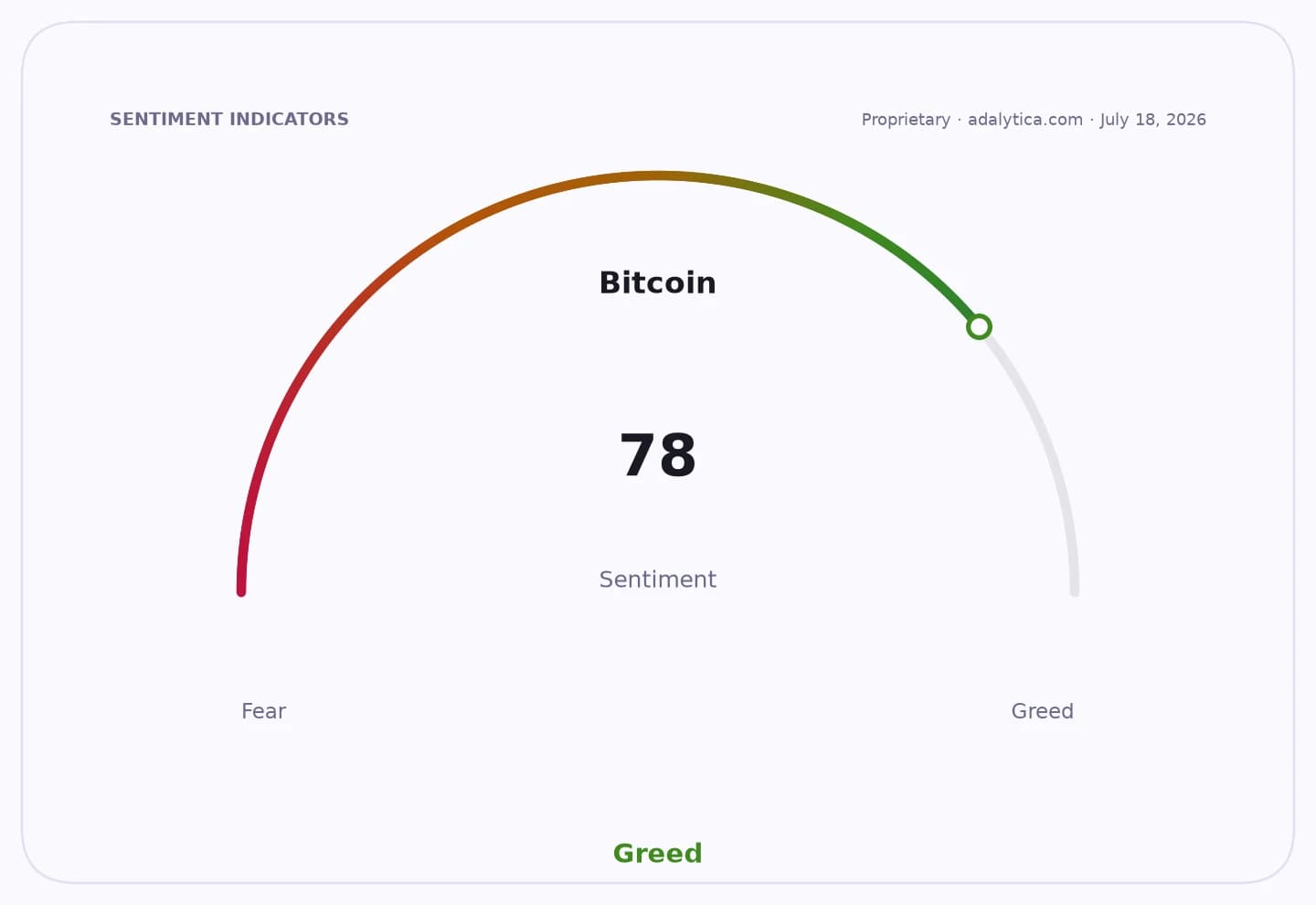

The timing is notable. Bitcoin has been trading with elevated volatility and is still far below its recent peaks, a reminder that crypto-related earnings can move quickly with market sentiment rather than fundamentals. SBI’s own shares have been volatile too, underscoring how much of the valuation case is tied to execution rather than immediate earnings uplift. Coinhako gives SBI a route into a fast-growing region, but the investment case will depend on whether the company can turn geographic reach into durable transaction volumes and not just headline exposure.

The broader narrative is that crypto is moving from a pure trading story toward a market-structure story in Asia. If SBI can use Coinhako to build scale in Singapore and adjacent markets, it may strengthen its role in regulated digital finance just as competitors, exchanges and payment firms compete for the same users. If adoption stalls or rules tighten unevenly across the region, the deal could end up looking like an expensive option on a still-fragmented market.

| Entity | Gains | Losses |

|---|---|---|

| SBI Holdings | ▲Southeast Asia growth platform | ▼Capital and execution risk |

| Coinhako | ▲Backing from a larger financial group | ▼Strategic independence |

| Crypto users in ASEAN | ▲More regulated access | ▼Fewer, stronger incumbents |

| Smaller crypto rivals | ▲— | ▼Pressure from a better-funded entrant |