Sticky inflation keeps rates on hold

Inflation is still rising, but only modestly, while growth and employment remain resilient enough to keep the economy expanding without forcing an abrupt policy shift.

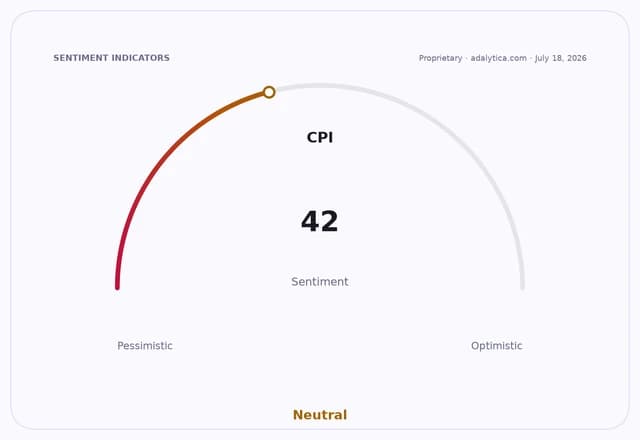

U.S. consumer prices are forecast to rise 0.89% in July, lifting the CPI to 335.512 from 332.568 in June, after a 0.42% decline the prior month. That suggests price pressures remain contained even as the economy keeps growing, with GDP projected to expand 1.54% in the second quarter to 32,358.0 after 1.41% growth in the first quarter.

For policymakers, that combination is the key macro story: inflation is no longer accelerating sharply, but it is not falling fast enough to justify easy money, while unemployment remains low at 4.18% in July from 4.2% in June. The data point to an economy that can still absorb higher rates, but not one that needs aggressive tightening either.

That is why markets are treating the inflation backdrop as a rate-hold story rather than the start of an easing cycle. The SPY has rebounded to 743.29, near its 50-day moving average of 743.23, while the S&P 500’s trade-signal snapshot from Adalytica shows neutral sentiment, even after a sharp one-day decline in the score. Financials have been among the clearer beneficiaries, with XLF at 56.26, well above both its 50-day and 200-day moving averages, reflecting expectations that banks can keep earning from still-firm growth and a high-rate environment.

Bond traders are less convinced the inflation path is fully settled. TLT finished at 84.52, below its 200-day moving average of 86.03, indicating yields are still being priced for a relatively restrictive policy stance. That split between equities and Treasuries captures the market narrative: growth is sturdy, inflation is moderating, and the Federal Reserve has room to wait.

The next catalyst is the July CPI print and the follow-up signals from labor-market data. If inflation comes in close to forecast while unemployment stays near 4.2%, investors are likely to keep betting on a prolonged hold, with winners in cyclical equities and financials and laggards in rate-sensitive bonds.

| Entity | Gains | Losses |

|---|---|---|

| Banks and financials | ▲Higher-for-longer rates | ▼Faster rate cuts |

| Equity bulls | ▲Stable growth backdrop | ▼Inflation reacceleration |

| Bondholders | ▲Slower inflation | ▼Sticky prices and yields |

| Consumers | ▲Cooler price pressure | ▼Wage gains lagging inflation |