Stocks Rally While Inflation Frustrates Voters

A blistering rally in U.S. equities is colliding with persistent inflation pressures, leaving many Trump voters split over whether the economy is working for them.

The tension matters because it goes to the heart of the political economy of the current expansion: asset owners have been rewarded, but households still face a higher price level than before the inflation surge that began in the early 2020s. The S&P 500 has climbed to about 7,575, more than 10% above its level in early June and far above where it stood before the pandemic, while consumer prices have continued to edge higher, with the CPI at 333.979 in May and forecast to rise another 0.62% in June. That combination helps explain why the market can look strong even as voters remain uneasy about affordability.

For investors, the split is important because it underscores a policy mix that is politically volatile and economically uneven. Equity holders are benefiting from resilient earnings, easing growth fears and a market that remains comfortably above its 50-day moving average. But the 10-year Treasury yield is still around 4.55%, keeping financing costs elevated and limiting how much relief reaches mortgages, auto loans and corporate borrowing. In other words, the stock market is signaling confidence, while rates and prices are still telling households a different story.

The message from the major asset classes is inconsistent but not contradictory. SPY has held above both its 50-day and 200-day moving averages, with the latest close at 754.95 and the 200-day at 691.09, a sign of a durable upward trend. Yet its recent RSI and MACD readings suggest the rally is no longer a one-way trade and is more vulnerable to any inflation surprise or rate scare. TLT, the long Treasury ETF, is still trading below its 200-day average, reflecting investor reluctance to bet on a decisive drop in yields. That leaves a classic split market: equities pricing growth and pricing power, bonds pricing sticky inflation and slower policy easing.

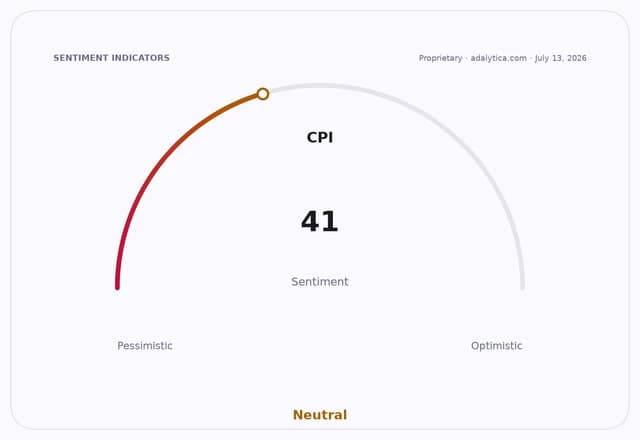

The inflation side of the ledger remains the more politically sensitive one. Even as the June CPI forecast points to a modest 0.62% monthly rise, the price level is far above pre-pandemic norms, which is what consumers feel at the checkout counter. That makes inflation a lingering grievance issue rather than a purely backward-looking macro statistic. The latest readings also explain why central banks, including the ECB in Europe, remain cautious about declaring victory despite cooling headline inflation in some economies. For U.S. voters, especially those who backed Trump on the promise of cheaper living costs, the disconnect between record-leaning markets and stubborn prices can sharpen frustration rather than relieve it.

The divide inside the Republican coalition is economically meaningful because it maps onto who captures gains from the boom. Wealthier households, retirees with equity exposure and higher-income voters are more likely to see the rally in portfolios, while lower-income consumers and borrowers are still absorbing the drag from elevated prices and rates. That can blunt the political payoff of rising stocks and leave the inflation narrative more durable than the market narrative.

The bull case for the economy is that inflation continues to cool gradually, allowing the Federal Reserve to ease later without derailing growth, and that strong markets signal confidence in corporate profits and productivity. The bear case is that the current setup reflects a narrow prosperity: equities rise, but real purchasing power improves only slowly, rates stay restrictive and voters judge the economy through grocery bills rather than index levels.

For investors, the next catalysts are straightforward: the June CPI print, the direction of the 10-year yield and whether the recent equity advance can hold if inflation data comes in hot. If prices keep moderating, stocks can extend their lead. If inflation reaccelerates, the market’s best recent story risks becoming a political liability again, especially among voters already split over whether Trump’s handling of the economy is delivering relief or just paper wealth.

| Entity | Gains | Losses |

|---|---|---|

| Equity investors | ▲Rising portfolio values | ▼Higher valuations risk |

| Cash-strapped consumers | ▲Possible later rate relief | ▼Persistent price pressure |

| Trump’s political coalition | ▲Supporters with stock exposure | ▼Voters focused on affordability |

| Treasury bulls | ▲Softer inflation prints | ▼Sticky yields |