Low-Deposit Aid Risks Negative Equity in Victoria

Thousands of first-home buyers in Victoria are facing the risk of negative equity after using the state’s low-deposit housing assistance scheme, a warning that could reshape how investors and policymakers view government-backed affordability programs.

The core issue is simple: when house prices stall or fall after a buyer enters with a small deposit, the loan can quickly exceed the property’s market value. That matters economically because it locks households into debt, weakens consumer balance sheets and raises the chance that stress in one part of the housing market spills into spending, lending and construction.

The threat is most acute in suburbs where prices have risen sharply on the back of assisted demand, leaving little cushion if conditions soften. For buyers, that can mean reduced mobility, harder refinancing and a greater burden if they need to sell. For lenders and insurers, it increases credit risk even if arrears remain low.

The broader policy problem is that low-deposit schemes can boost access without increasing supply fast enough. If new homes and affordable stock do not keep pace, assistance programs can inflate prices in the very areas they are meant to open up, pushing the weakest buyers onto the thinnest financial footing.

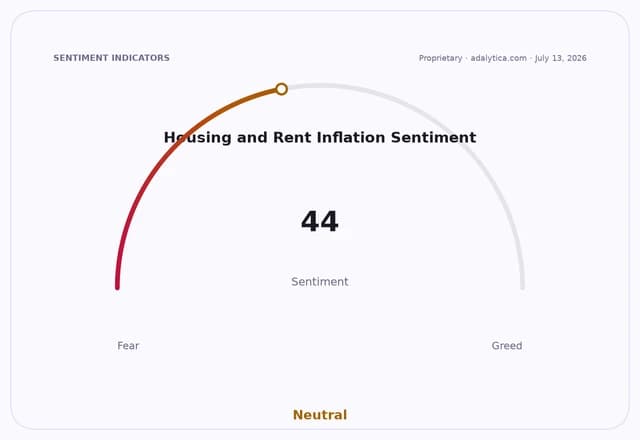

For investors, the story is a reminder that housing support is not the same as housing stability. Builders, lenders and real-estate-linked funds remain exposed to policy-driven demand, but that demand can reverse quickly if affordability concerns, higher borrowing costs or falling prices hit confidence. The XHB housing gauge is still flashing strong appetite, but conventional technical indicators and the recent spike in housing sentiment suggest the market may be more vulnerable to a pullback than it looks.

The next catalyst is whether authorities tighten eligibility, expand supply or redesign the scheme to reduce the chance that subsidized buyers become trapped in under-water mortgages. If they do not, more households could find themselves owning homes they cannot easily sell, and the political cost of the policy could rise just as quickly as the housing market did.

| Entity | Gains | Losses |

|---|---|---|

| First-home buyers with access to the scheme | ▲Lower deposit hurdle | ▼Negative-equity risk |

| State government/policymakers | ▲Short-term homeownership wins | ▼Policy backlash if prices weaken |

| Banks and lenders | ▲More mortgage originations | ▼Higher credit-risk exposure |

| Homebuilders in supported suburbs | ▲Demand boost | ▼Risk of slowdown if scheme is revised |